DON’T FEAR A STRONG START TO THE YEAR

It’s April 1, and the first quarter of 2024 is in the books. On the heels of more than 25% in total return for 2023, the S&P 500 returned more than 10% in the first quarter. The logical question is: How much is too much? Looking at the numbers, more good news could be in store for the bulls.

- 2024 is off to a strong start. The first three months of the year have been positive, marking a five-month streak of stock market wins.

- Strong starts to the year typically lead to above-average performance over the rest of the year.

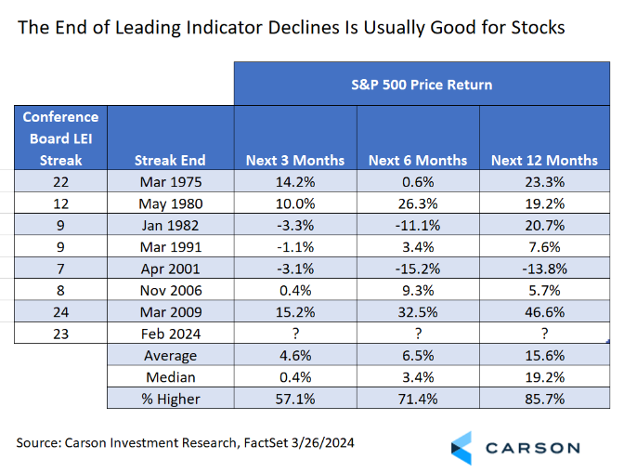

- The Conference Board’s widely followed Leading Economic Index finally had its first monthly gain after 23 consecutive months of declines.

- The end of long declines has typically been bullish for stocks.

- Carson’s proprietary leading index, which pays more attention to consumer spending patterns and never signaled a recession, continues to have a more optimistic outlook than The Conference Board.

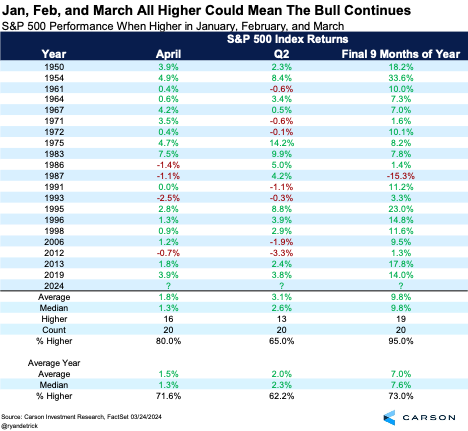

Stocks have ended each of the first three months of 2024 higher. When this has happened in the past, the final nine months of the year have been higher an incredible 19 out of 20 times! Adding to the fun, April and the second quarter also tend to do better than average.\\

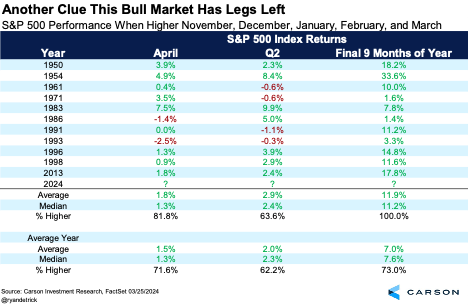

Let’s not forget stocks soared in November and December, so they are up five months in a row heading into the usually bullish month of April. Sure enough, stocks tend to do better in April and the second quarter after such long win streaks. Lastly, the rest of the year has never been lower when there has been at least a five-month win streak heading into April.

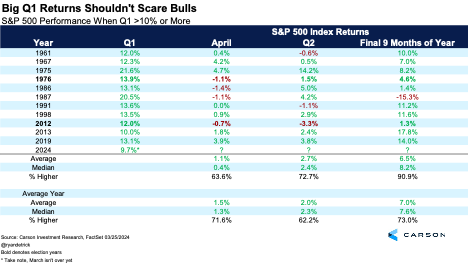

What about when the first quarter gained 10% or more? April and the second quarter did not perform especially well, but the rest of the year was higher 10 out of 11 times. The market was only lower in 1987. During that year, the market rose a record 20.5% by the end of the first quarter, which is a little different than the approximately 10% gain so far in 2024. The average took a big hit those final nine months due to the 1987 stock market crash, but the median was a rather solid 8.2%.

Looking more closely at the data above, we noticed only 1976 and 2012 were election years and the market returned 4.6% and 1.3%, respectively. Returns weren’t really about the elections, but it’s worth keeping in mind.

Lastly, there has been broad-based participation in this rally. Many large institutional research shops continue to (incorrectly) claim that only a few technology-oriented stocks are pulling the market higher. This isn’t true and never was, especially with Apple and Tesla losses in 2024 taking some of the shine off the Magnificent Seven.

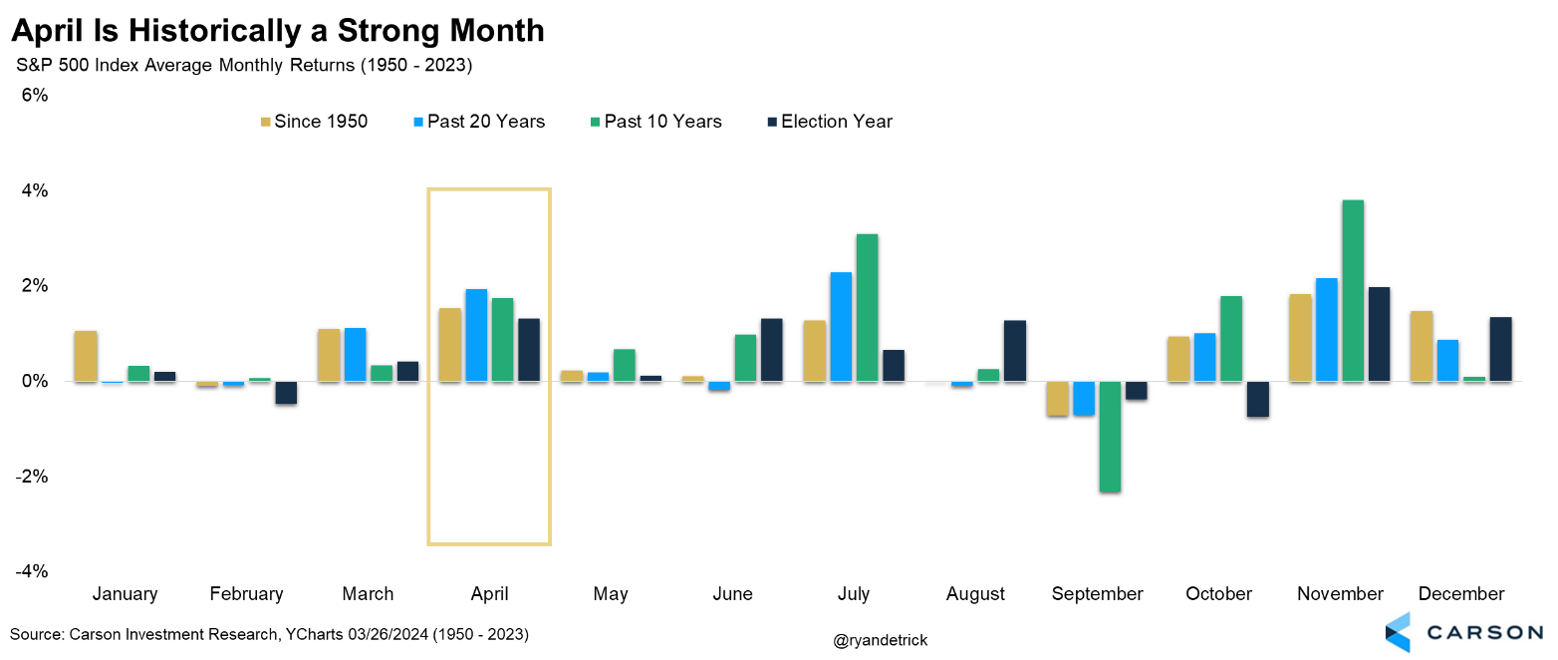

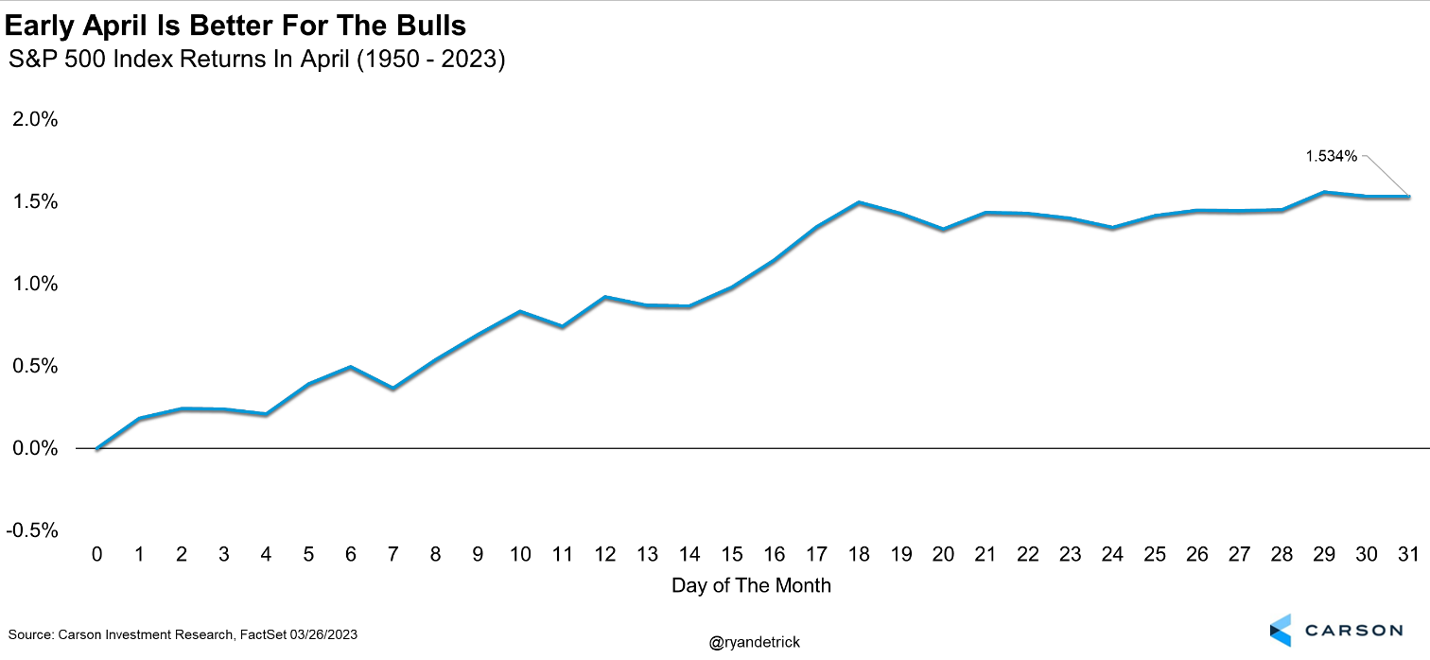

APRIL A HISTORICALLY STRONG MONTH

The S&P 500 has averaged 1.5% in April, the second best month of the year (only November is better). April has also been the third best month over the last 10 years, and it has been the fourth best month over the last 20 years and during election years.

Be aware that much of the gains in April historically take place during the first part of the month.

As long-time followers of this commentary know, we’ve been quite bullish on both the stock market and the economy for well over a year now. Could stocks fall in April? Sure, after the run we’ve had anything is possible. But the odds favor more green numbers.

RIVAL LEADING INDICATORS CATCHING UP WITH THE ECONOMY

Probably the most watched leading indicator, The Conference Board’s Leading Economic Index, had a monthly gain for the first time in almost two years in its most recent release. After 23 consecutive months of month-over-month declines, the LEI finally inched higher, granted by the smallest of margins, gaining 0.1%. Throughout the current rally, we have deferred to our proprietary leading economic index, created by our Chief Macro Strategist Sonu Varghese, whose Ph.D. in engineering doesn’t literally make him a rocket scientist (his work was in fluid dynamics), but close enough for us.

Our leading indicators not only cover the U.S. but all major economies based on their individual economic sensitivities, which we can then roll up to regional and global leading indicators. While our U.S. indicator showed elevated risk compared to the average back in 2022, it was not signaling a recession. Rather, it pointed to something closer to a mid-cycle slowdown, which is in line with what actually happened.

Right now, our U.S. leading indicator, shown below, is signaling on-trend growth for the rest of the year, supported by cyclical areas of the economy. The Conference Board continues to see growth slowing to below-trend after announcing that its LEI is no longer signaling a recession just last month. Of course, even that’s a big improvement over those economists who continuously repeat that a recession is coming, with the timing pushed out every time they are wrong. Do that for long enough (and it’s been long enough), and they’re in “even a broken clock is right twice a day” territory.

Considering the market impact, there have been only two streaks of LEI monthly declines similar to the one we just broke — a 22-month streak ending in March 1975 and a 24-month streak ending in March 2009. Only five other streaks have lasted as long as six months and none longer than a year.

These streaks don’t mean much on their own. It’s the change in the index over time that matters, and there may be occasional positive months. But the two previous streaks that lasted around two years did correspond to longer recessions, so they aren’t without meaning. The end of the 22-month streak in 1975 coincided with the end of a 16-month recession, while the end of the 24-month streak in 2009 came just three months before the end of the Great Recession, which lasted 18 months. Compare that to the average post-WWII recession of just over 10 months.

It is noteworthy that the end of these two longer streaks corresponded to the end of some longer recessions. That gives us added confidence that we are past near-term recessionary risk. After the end of the two previous long streaks, the S&P 500 returned an average of 34.9% over the next year, although circumstances were quite different. The end of all LEI declines of at least six months shows an average of more than 15%.

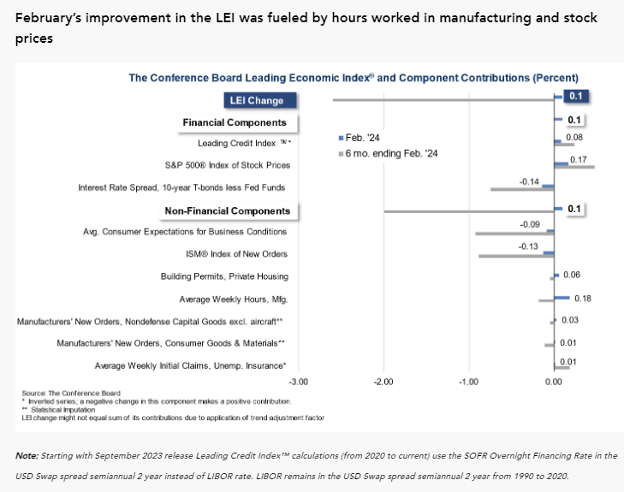

Even though the streak is over, it doesn’t take much to get a 0.1% lift, even if the markets haven’t managed that in a while. As shown below, most subcomponents were flat to moderately positive in February. Over the last six months, the biggest drag continues to be consumer expectations, manufacturing purchasing managers’ expectations of new orders, and the yield curve. That’s two survey-based readings and elevated short-term rates due to inflation, which has declined quite a bit, rather than an overheated economy.

The bottom line is that no matter which indicators you pay attention to, economic headwinds are slowly being taken out of play. Despite a strong first quarter for equities and the likelihood of bumps along the way, the outlook for stocks over the rest of the year still looks solid, whether considering the macroeconomic backdrop or, as discussed above, market history.

This newsletter was written and produced by CWM, LLC. Content in this material is for general information only and not intended to provide specific advice or recommendations for any individual. All performance referenced is historical and is no guarantee of future results. All indices are unmanaged and may not be invested into directly. The views stated in this letter are not necessarily the opinion of any other named entity and should not be construed directly or indirectly as an offer to buy or sell any securities mentioned herein. Due to volatility within the markets mentioned, opinions are subject to change without notice. Information is based on sources believed to be reliable; however, their accuracy or completeness cannot be guaranteed. Past performance does not guarantee future results.

S&P 500 – A capitalization-weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

The NASDAQ 100 Index is a stock index of the 100 largest companies by market capitalization traded on NASDAQ Stock Market. The NASDAQ 100 Index includes publicly-traded companies from most sectors in the global economy, the major exception being financial services.

A diversified portfolio does not assure a profit or protect against loss in a declining market.

Compliance Case # 02179795_040124_C